Something has been changing in how people actually pay for things, and it does not show up dramatically in headlines. It shows up in the behavior of freelancers, digital advertisers, small business owners, and privacy-conscious consumers who have quietly stopped relying on traditional bank-issued debit and credit cards for a growing share of their transactions.

Prepaid cards sit in an interesting structural position. They are not bank accounts. They carry no credit line. They impose no overdraft risk. And increasingly, they offer capabilities that traditional cards simply do not, particularly for anyone operating across platforms, borders, or payment ecosystems that banks treat with friction or suspicion.

The technical mechanics that matter

A prepaid card functions on a stored-value model. The issuer holds funds in a pooled or segregated account, and the card draws down against that balance. Most modern prepaid virtual cards run on Visa or Mastercard rails, which means merchant acceptance is effectively global. The BIN (Bank Identification Number) on the card determines how processors classify it, and some providers carefully manage BIN selection to optimize for specific use cases, such as ad platforms, which have historically blacklisted BINs associated with high chargeback rates.

One technical distinction that rarely gets explained clearly is the difference between reloadable and single-use prepaid cards. Reloadable cards maintain a persistent balance and can be topped up repeatedly. Single-use or disposable virtual cards generate a unique card number for one transaction and then become inactive. The latter essentially eliminates the category of fraud that involves harvesting stored card credentials, because there are no credentials worth harvesting after the transaction completes.

3D Secure (3DS) authentication adds another layer. When a card supports 3DS2, the issuing bank or prepaid operator can pass device fingerprinting, behavioral data, and session context to the merchant’s payment processor during authorization. This raises approval rates on legitimate transactions while flagging anomalies. For users who run volume across digital platforms, the quality of the 3DS implementation directly affects transaction success rates.

Funding method diversity is another axis where prepaid operators have outpaced traditional banks. SEPA and SWIFT transfers cover the conventional banking layer, but accepting USDT on TRC20 and ERC20, Bitcoin, Ethereum, and other chains means that users with crypto treasury positions can fund their spending without converting through an exchange first. This is operationally significant for any team that holds working capital in stablecoins.

Who actually uses these cards and for what

The clearest use case is digital advertising. Meta, Google, TikTok, and similar platforms charge cards automatically, often with unpredictable timing. A media buyer managing multiple ad accounts needs cards that can be individually capped, easily replaced if declined, and separated by client or campaign. Issuing one card per account is standard practice in serious performance marketing operations.

The second major use case is SaaS and subscription management. Businesses running dozens of software subscriptions benefit from assigning dedicated cards to each vendor. If a vendor is compromised or starts billing incorrectly, the card can be frozen or deleted without affecting anything else.

A third use case is cross-border commerce. Consumers purchasing from merchants in different jurisdictions encounter currency conversion fees, foreign transaction fees, and occasional outright blocks from domestic banks. Prepaid cards denominated in USD or EUR sidestep many of these issues, particularly when the issuer does not charge foreign transaction fees.

Prepaid card services: a factual ranking

The three services below represent different approaches to the same core problem: giving users a payment instrument that a bank card cannot cleanly provide. Each one addresses a specific friction point, and understanding which friction point matters most helps identify which service actually fits a given use case.

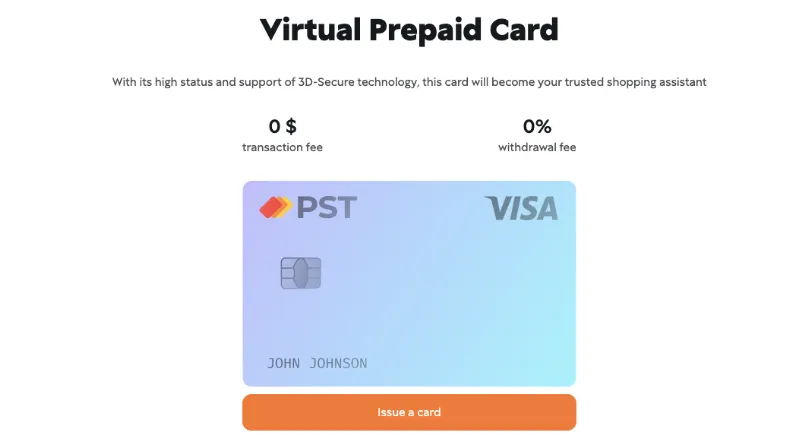

1. PSTNET

PSTNET is the most structurally complete option on this list for anyone who needs to separate spending by purpose rather than by account. The platform issues different card types for different tasks, which is the key differentiator. For example, a user looking for an online prepaid card for advertising spend gets a dedicated card with cashback built in. General online purchases get their own card category. This is not cosmetic segmentation; it reflects genuine BIN management where each card type is optimized for the merchant category it targets.

The funding model reinforces that logic. Users deposit into a central balance inside the dashboard and then allocate specific amounts to individual cards. Nothing moves to a card until the user decides it should, which means the exposure on any single card is always bounded. This is exactly the kind of control that a bank card connected to a primary account cannot provide.

On the cost side, PSTNET charges no transaction fees, no withdrawal fees, and no fees on operations involving declined cards. That last point is practically significant: declined transaction fees are a hidden cost on many prepaid platforms that eats into budgets silently. First deposits made in USDT are processed without commission, which matters for teams already holding stablecoin balances.

Funding options span SEPA and SWIFT bank transfers, Visa and Mastercard top-ups, and 18 cryptocurrencies including Bitcoin, Ethereum, and USDT on both TRC20 and ERC20 networks. Security runs on 3D Secure with two-factor authentication layered on top. Registration takes a few minutes using Google, Telegram, WhatsApp, Apple ID, or email, and requires only a passport for verification. Card management and transaction notifications are available through a mobile app and a Telegram bot, with 24/7 support accessible via Telegram and other messaging platforms.

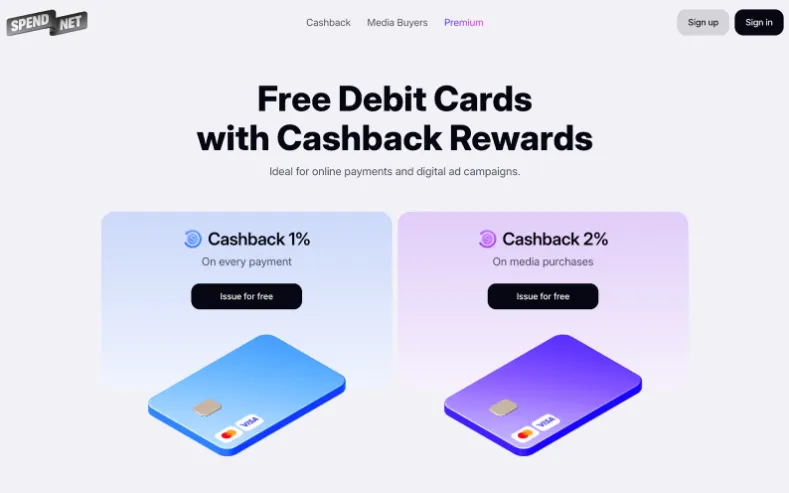

2. Spend.net

Spend.net approaches the alternative-to-bank-card problem from a slightly different angle. Where PSTNET emphasizes card type segmentation and broad funding options, Spend.net keeps the infrastructure lean and makes cashback the primary financial incentive for switching from a conventional card. The two percent return on advertising spend and one percent on other online purchases is a direct answer to the question of why a user would replace their bank card: the economics of doing so are better.

Card issuance costs nothing, and activation is immediate once the account is funded. Spend.net onboarding requires only an email address or a Google login, which reduces the barrier for users who want to test the service before committing. The funding constraint is worth noting: Spend.net accepts only Bitcoin and USDT on TRC20, so users without a crypto position need to acquire one first. For teams already operating with digital asset balances, this is not a friction point. For users coming entirely from the traditional banking layer, it is.

The analytics and reporting tools address a gap that bank cards handle poorly. Most bank statements group transactions by merchant name with minimal categorization. Spend.net provides budget analytics with export options in CSV and XLS formats, which integrates directly into accounting workflows. Every transaction runs through 3D Secure, and live chat support is available around the clock on the platform website.

3. Revolut

Revolut occupies a different position in this comparison. It is less a pure prepaid service and more a multi-currency account with prepaid card functionality built in, which makes it the most appropriate option for users whose primary friction with bank cards is cross-border spending rather than platform or account separation.