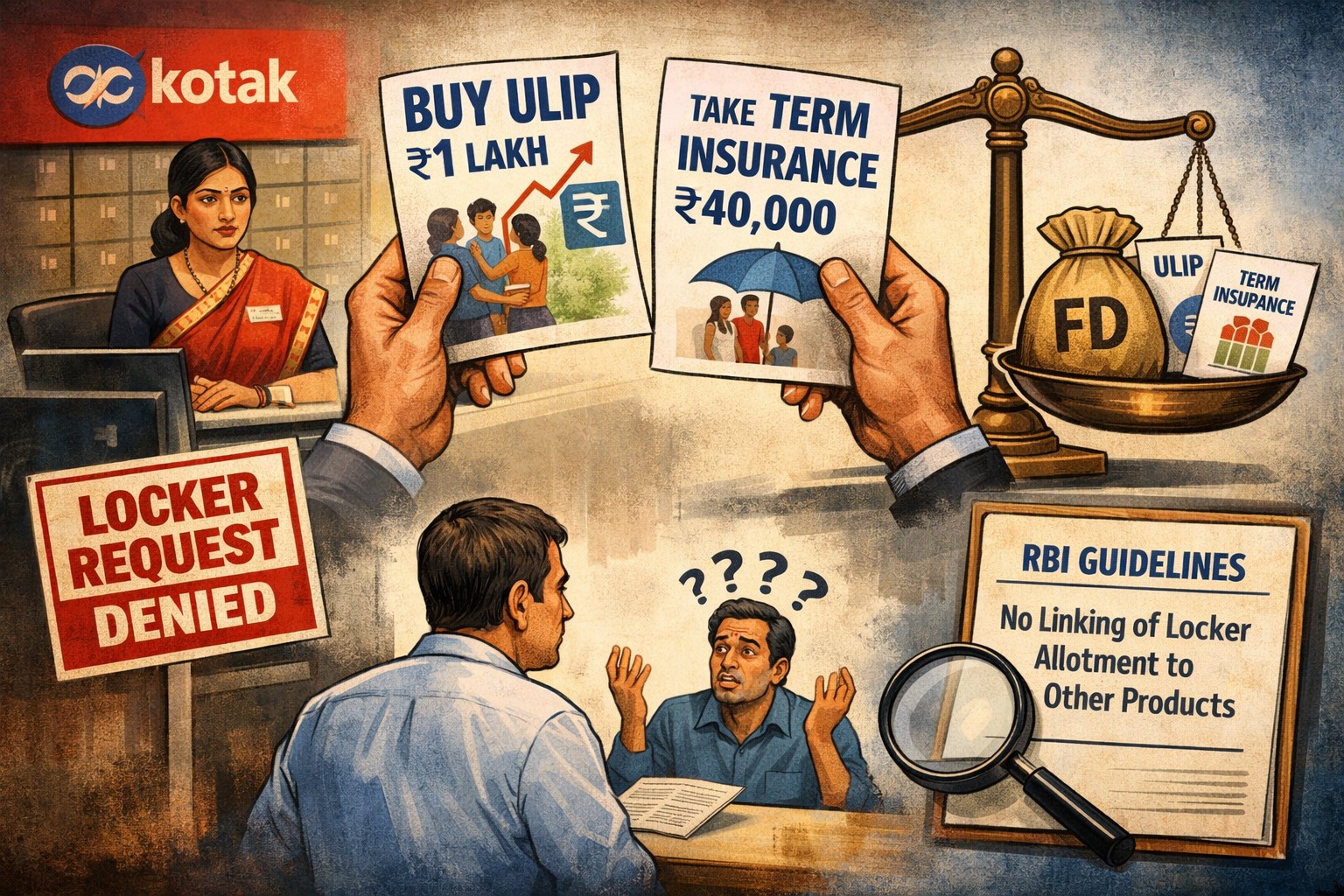

Kotak Mahindra Bank Faces Backlash for Violating RBI Guidelines After Customer Denied Locker Without Insurance

Related Articles

MEA Refutes NYT Report, Says Musk Was Not On Modi-Trump Call

The Ministry of External Affairs on Saturday firmly denied a report suggesting that Tesla CEO Elon Musk was part of a recent telephonic conversation...

Amid Oil Market Volatility, Russia To Ban Gasoline Exports From April 1

Russia has announced a ban on gasoline exports starting April 1, in a move aimed at stabilising domestic fuel prices and ensuring adequate supply...

Adani Delivers First 2,000 Prahar LMGs To Armed Forces, Ahead Of Schedule

Adani Defence and Aerospace, in partnership with Israel Weapon Industries (IWI), on Saturday delivered the first batch of 2,000 Prahar Light Machine Guns (LMGs)...