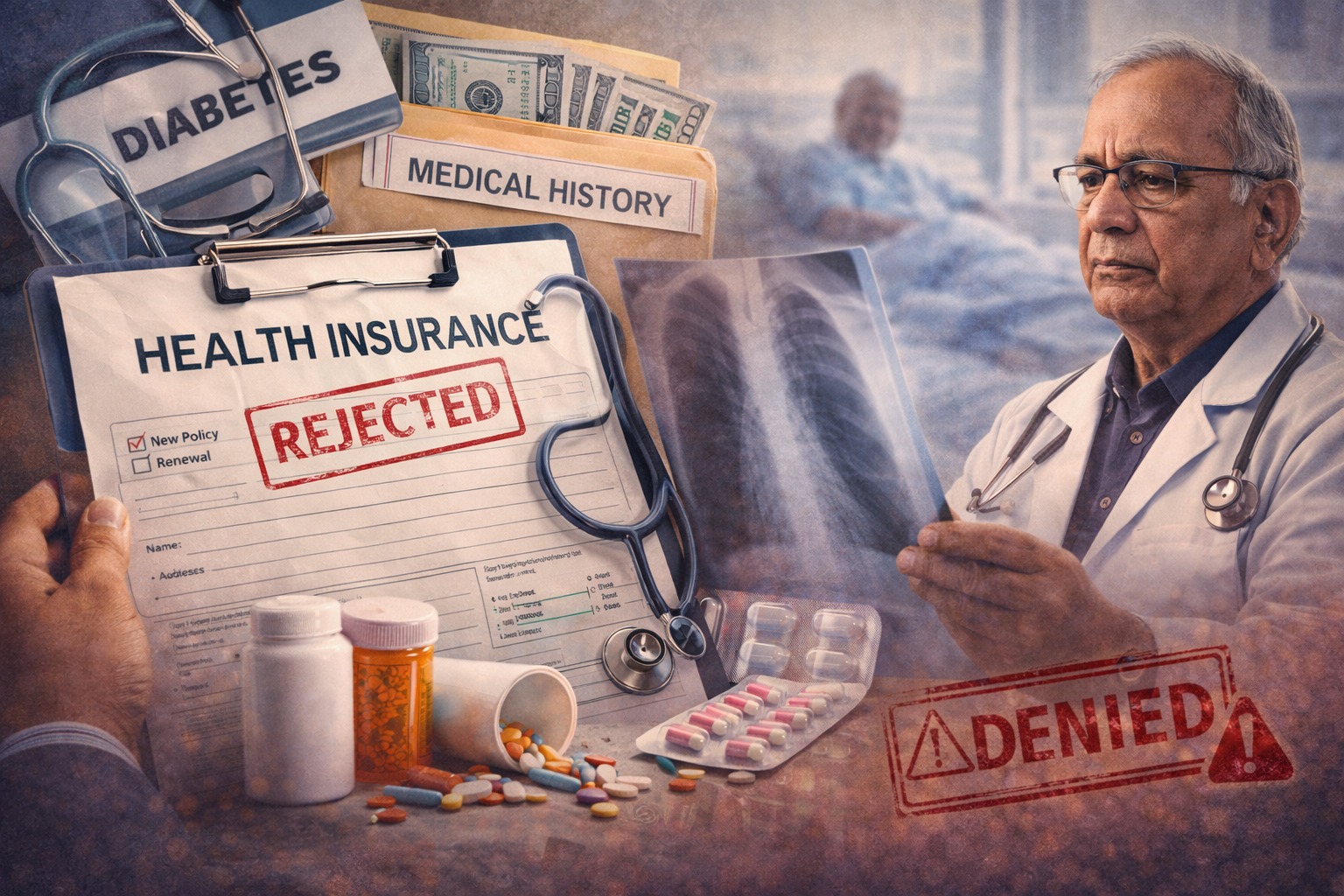

Concealing Pre-Existing Conditions in Health Insurance: A Risky Move

Related Articles

Rajya Sabha Passes CAPF Bill Amid Opposition Walkout

On April 1, the Rajya Sabha approved the Central Armed Police Forces (General Administration) Bill, 2026, through a voice vote, coinciding with a walkout...

Gujarat’s District Level Sports School Scheme Equips Athletes for Competitions

Launched by Prime Minister Narendra Modi during his tenure as Chief Minister, the District Level Sports School (DLSS) scheme aims to foster discipline, sportsmanship,...

Parliament Budget Session Set to Reconvene in April, Government Plans Key Legislative Changes

The Indian Parliament's Budget Session is expected to resume in the third week of April, contrary to earlier indications of a sine die adjournment...